The European Kombucha Market in 2026: What You Need to Know

Europe's kombucha market reached approximately €905 million (USD 1.02 billion) in 2025, growing at around 13.4% annually.

But here's what makes Europe fundamentally different from North America: 60% of Europeans still don't know what kombucha really is.

That's not a problem. It's an opportunity. Of those unfamiliar with kombucha, 85% say they'd like to try it. The category is nowhere near saturated. Early movers have runway that North American brands no longer enjoy.

The other critical difference? European consumers discover kombucha through cafés, bars, and restaurants first, then buy it for home. That's the opposite of North America's retail-first journey. It changes everything about how brands need to build awareness and distribution.

This breakdown walks through what's actually happening in the European kombucha market heading into 2026. The consumer shifts, regional dynamics, competitive landscape, and opportunities that matter if you're building or growing a brand in Europe.

Download our free 2026 Global Kombucha Report for exclusive insights into shifting consumer habits, regional trends, and the production strategies that will help you capture the next wave of growth.

Market Size Across Europe

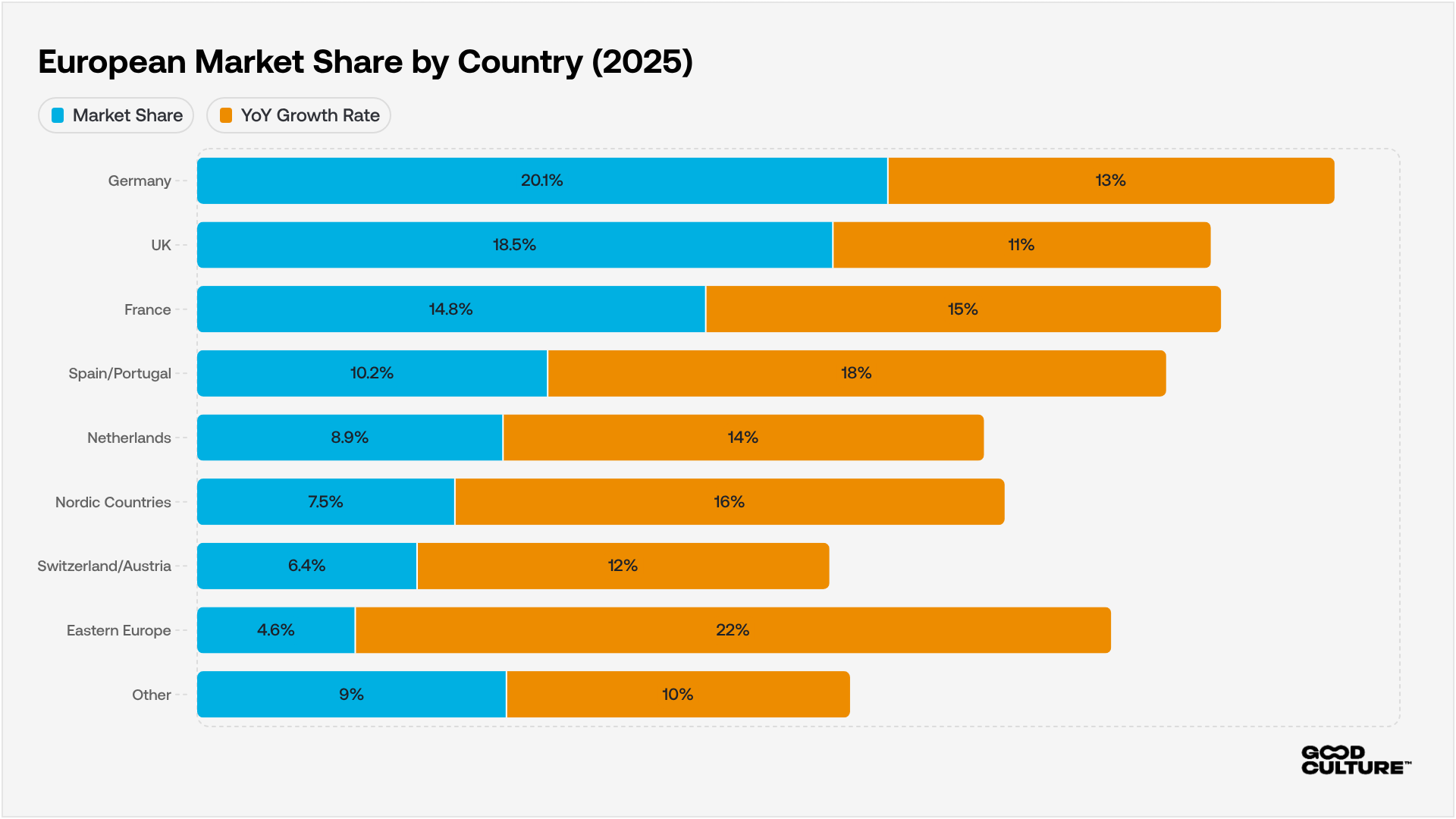

Europe's kombucha market reached approximately €905 million in 2025. Germany dominates with 20.1% revenue share. The UK and France follow as the fastest-growing markets, with France projected to hit USD 379 million by 2033, up from USD 108 million in 2024.

Hard kombucha is the fastest-growing segment. It's projected to grow at 17.8% CAGR from 2025 to 2033. That compares to 13.4% for conventional kombucha. The gap matters. It signals where European consumer interest is accelerating, particularly in the UK and Germany where hard kombucha has genuinely taken hold.

But the biggest shift isn't in the numbers. It's where kombucha is being consumed and who's driving adoption. And that story looks nothing like North America.

The Café Discovery Model That Defines European Kombucha

Here's the critical difference between European and North American markets. Café and hospitality channels account for 60.8% of European kombucha distribution in 2024. That's not just higher than North America. It's a fundamentally different business model.

European consumers discover kombucha on-tap at London gastropubs, Berlin cafés, and Parisian bistros. They try it in a social setting first. If they enjoy it, they seek it at Tesco, Carrefour, or their local organic shop. That journey (hospitality discovery → retail purchase) is the opposite of North America's retail-first model where consumers discover brands in Walmart coolers.

This changes everything about market strategy. Brands that secure café and bar placement generate awareness that drives retail sales. Brands going straight to retail without hospitality presence struggle to build consumer familiarity in markets where 60% of people still don't know what kombucha is.

The UK leads this model. Kombucha-on-tap in London pubs and coffee shops has normalised the category for consumers who'd never set foot in a health food store. France follows close behind. Parisian cafés position kombucha as a sophisticated alternative to wine and champagne, particularly amongst younger demographics seeking refined refreshment without alcohol.

Germany's café scene is slightly different. Berlin and Munich cafés emphasise kombucha's health benefits and organic credentials ("bio," "vegan," "locally sourced"). These certifications matter enormously. Germany's organic food market generates over €1.6 billion annually, creating a consumer base that genuinely understands and values certified organic kombucha.

For brands targeting European markets, hospitality isn't a nice-to-have. It's the primary discovery channel. Build those relationships first. Retail follows.

How European Consumers Think About Kombucha

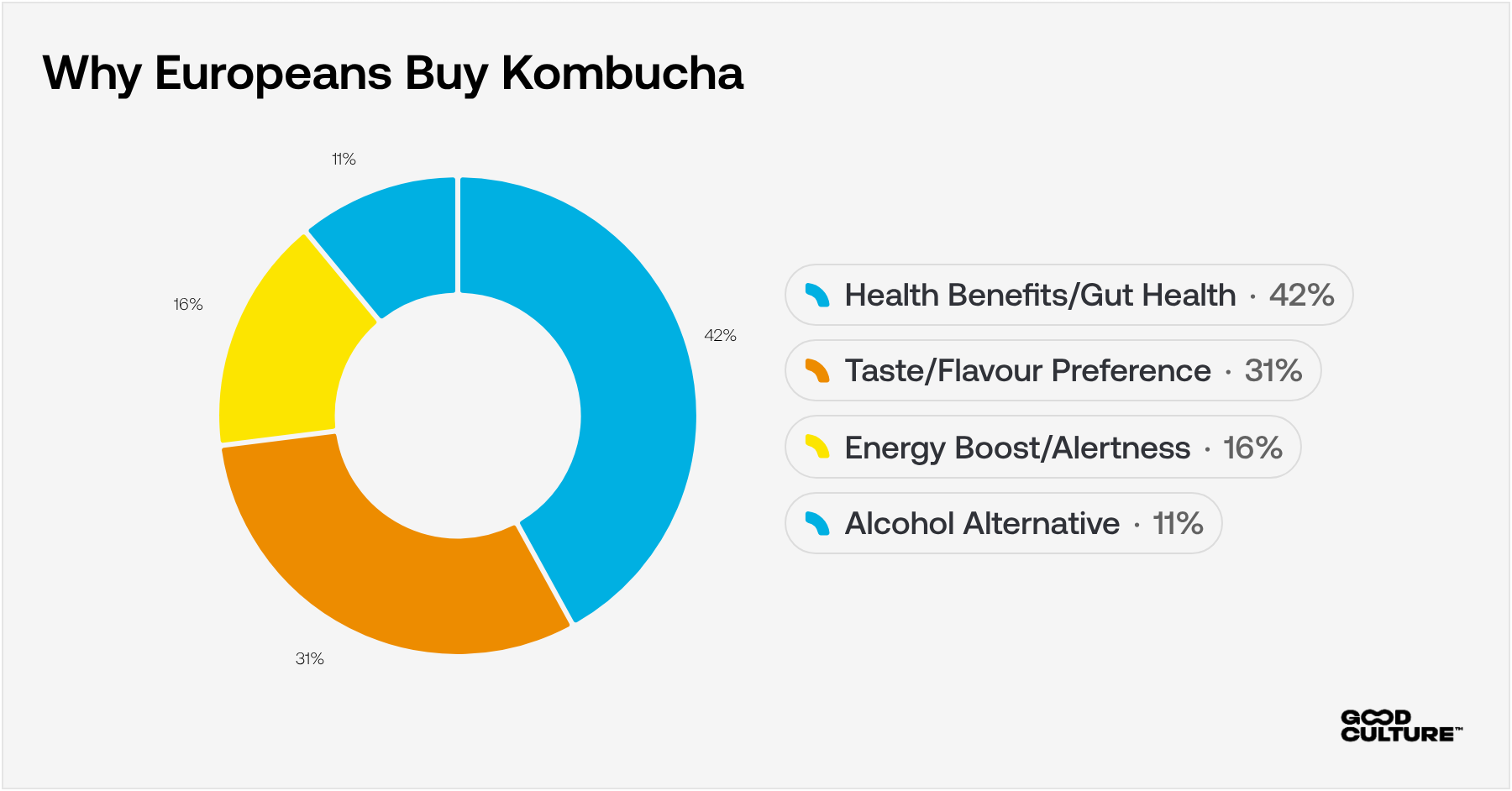

European purchase motivations differ from North America in important ways. Health benefits remain the primary purchase driver at 42%. That's significantly higher than North America, where taste and curiosity now lead. European consumers discovering kombucha are still coming through wellness channels. They want probiotics, gut health, and digestive benefits.

But taste is rising fast at 31%. As the category matures and discovery shifts from health food stores to mainstream cafés, European consumers are becoming more like their North American counterparts. They're choosing kombucha because it tastes good and happens to offer health benefits, not the other way around.

The alcohol alternative positioning (11%) is particularly strong in the UK. British consumers seeking low-alcohol functional options to cider and beer are driving adoption beyond traditional wellness demographics. Hard kombucha's success in UK pubs has created a halo effect. Non-alcoholic kombucha benefits from this normalisation.

Ready for 2026? Download the Global Kombucha Report for the trends, tactics, and insights you need to future-proof your brand.

Age Demographics Differ Dramatically by Country

Here's where European markets diverge from each other and from North America.

In Germany, kombucha targets adults aged 30-50. These consumers understand health benefits and can afford premium pricing (€3.50 to €4.50). They respond to "bio" certification, vegan credentials, and locally-sourced ingredients. German millennials are less central to the story than middle-aged health-conscious consumers with disposable income.

In the UK, millennials and Gen Z drive adoption. Younger British consumers discover kombucha through trendy London cafés and boutique grocers like Whole Foods. They're seeking Instagram-worthy beverages and alcohol alternatives for social settings.

In France, the target skews younger but sophisticated. Parisian café culture introduces kombucha to 25-40 year olds who view it as a refined alternative to wine. Michelin-starred chefs incorporating kombucha into tasting menus elevates its status beyond functional beverage into gourmet territory.

These aren't subtle differences. They're fundamental divergences that require different positioning, packaging, and distribution strategies by country.

Regional Growth Patterns Across Europe

Germany has been Europe's largest kombucha market for 35 years. Despite this maturity, it's still seeing double-digit growth as health and wellness trends accelerate. But Germany remains fundamentally niche. The market is growing, but it's not mainstream the way North American kombucha has become.

France is emerging as the fastest-growing market. That 15% CAGR reflects kombucha's unique positioning in French culinary culture. It's not just a health drink. It's a sophisticated beverage alternative that fits naturally into café and restaurant settings where French consumers spend significant time socialising.

Eastern Europe (Czech Republic, Poland, Romania) represents frontier opportunity. These markets show 22% growth despite low awareness. Urbanisation and rising disposable incomes are creating conditions for rapid adoption. Brands entering early with affordable pricing and local distribution partnerships can establish dominant positions before Western European brands expand eastward.

Spain benefits from government subsidies for small-scale producers. This has fostered innovation and affordability. Barcelona and Madrid have emerged as kombucha hotspots, with cafés and speciality stores offering unique tropical flavours (mango-pineapple, coconut-lime) that differentiate Spanish brands from Northern European competitors.

Nordic countries show 16% growth driven by sustainability-conscious consumers. Swedish, Norwegian, and Danish consumers prioritise environmental responsibility. Brands offering can packaging (90% less energy to recycle than glass) and transparent supply chains resonate strongly in these markets.

Pricing Dynamics in European Markets

Premium brands command €3.50 to €4.50 in natural retailers and speciality stores. They're doing fine in their lane. But volume is happening at €2.00 to €2.99. Brands like Remedy (€2.49 to €2.79), GUTsy Captain (€2.50 to €2.99), and private label (€1.99 to €2.49) are taking share rapidly across European mainstream retail.

Research shows sharp demand elasticity around €3.00. Above that threshold, purchases become deliberate decisions requiring justification. Below it, beverages enter impulse territory.

But here's the European nuance that doesn't apply in North America. Premium positioning still works brilliantly in on-trade. European cafés, bars, and restaurants charge €4.00 to €5.00 per bottle because the consumption context justifies premium. Consumers accept café pricing they'd never pay in a supermarket.

The bifurcation is channel-specific. Retail demands value. Hospitality accepts and expects premium. Brands need different pricing strategies for each channel, not uniform pricing across distribution.

The Functional Soda Threat Is Coming (But Hasn't Landed Yet)

Functional sodas haven't yet disrupted European markets the way Olipop and Poppi transformed North America. But the window is closing.

PepsiCo acquired Poppi in 2025 for USD 1.95 billion. That signals serious capital being deployed for global expansion. Europe is the obvious next target after North America saturation. Olipop launched shelf-stable versions in August 2024, removing refrigeration constraints that limit European retail distribution.

Both brands are entering UK and German markets with aggressive positioning. They offer 2-5g sugar per can, similar gut health claims, taste closer to mainstream soda, and retail at €2.29 to €2.79.

But here's Europe's advantage. European kombucha's authentic fermentation story, live cultures (in unpasteurised versions), and centuries of tradition are defensible differentiators. Functional sodas can't replicate these. They offer prebiotics (food for good bacteria), not actual live cultures from fermentation.

European consumers, particularly in Germany and France, value authenticity and traditional production methods more than North American consumers do. The "bio" certification obsession in Germany, the culinary sophistication in France, the artisanal appreciation across Nordic countries create natural defences against mass-market American functional sodas.

Brands that articulate this difference clearly ("We're actually fermented. They're soda with fibre added.") will capture consumers before Olipop and Poppi establish European beachheads. But they need to move now. The threat is real, and it's coming fast.

For detailed formulation strategies, see how to formulate low-sugar kombucha without sacrificing flavour.

Hard Kombucha's Gateway Effect in Europe

Hard kombucha reached approximately €55 million in Germany alone, growing at 40-45% annually across Europe. The broader European market is projected to reach USD 1.5 billion by 2031.

The gateway effect is real and measurable in Europe. Hard kombucha introduces millions of consumers annually who then purchase non-alcoholic versions for everyday consumption. This is particularly pronounced amongst males aged 25-45, a demographic traditionally underrepresented in non-alcoholic kombucha.

Major European hard kombucha brands (Flying Embers, Remedy, Ummi) are normalising kombucha for consumers who'd never visit health food stores. When those consumers enjoy hard kombucha at a Berlin brewery or London bar, they're more likely to buy regular kombucha at their Tesco or Carrefour.

The UK leads this trend. British pub culture creates natural distribution for hard kombucha. That hospitality presence generates awareness that spills into retail demand for non-alcoholic options.

What European Retailers Want from Brands

Conversations with UK, German, and French retail buyers reveal expectations that differ subtly but importantly from North American demands.

Consistency. When Tesco stocks your SKU in 300+ stores, they need confidence every bottle tastes the same. One bad batch means delisting conversations. This is universal. But European retailers remember supplier problems longer than American buyers do. Reliability matters more than novelty in markets where turnover decisions are slower and more deliberate.

On-trade integration. This is uniquely European. Buyers at Carrefour and Sainsbury's increasingly value brands with strong café, restaurant, and bar placement. When Remedy or GUTsy Captain appear on Parisian café menus or London gastropubs, their supermarket facings strengthen. Cross-channel presence signals brand credibility and consumer demand in ways North American buyers don't prioritise.

Clean compliance with varying national laws. Most of Europe requires 0.5% ABV. But some Nordic countries and Spain allow 1.2%. Germany has stricter organic certification requirements than France. The UK post-Brexit has slightly different labelling rules than EU countries. Navigating this complexity requires more sophisticated compliance systems than the relatively uniform North American market.

For detailed guidance on staying compliant across European markets, see how to control alcohol in commercial kombucha production.

Competitive pricing that protects retail margin. Products under €3.00 move measurably faster than products over €3.50. But European retailers also want brand partners who protect retail margin through controlled distribution, not ones constantly discounting to compete. The balance is delicate and market-specific.

Trends Reshaping European Kombucha in 2026

Cans Gaining Ground in Retail (Glass Dominates Hospitality)

European consumers, particularly in Germany, UK, and Scandinavia, prioritise sustainability. Aluminium recycles at 90% less energy than glass. Brands offering can-primary lineups appeal to environmental consciousness that glass-focused competitors can't match.

But glass bottles remain preferred in European on-trade. In cafés, restaurants, and bars, glass signals premium and artisanal positioning. The can transition will be faster in retail than hospitality.

Low-Sugar Without Compromising Authenticity

Research shows 76% of Europeans actively limit sugar. Traditional kombucha at 6-10g sugar per 100ml creates cognitive dissonance.

But here's the European nuance. Unlike North America, where "low-sugar" often means any sweetener that reduces sugar count, European consumers demand "low-sugar without compromising authenticity." Stevia, erythritol, and monk fruit are acceptable. Aspartame and acesulfame K generate immediate scepticism.

European brands must communicate not just what sugar they've removed, but what natural ingredients they're using instead and why those align with European quality expectations (particularly Germany's "bio" standards).

Regional Flavours are Rooted in Culinary Traditions

Mediterranean profiles (hibiscus-pomegranate, olive-lemon) resonate in Southern Europe. Northern flavours (lingonberry-spruce, elderflower-Nordic herbs) perform in Scandinavia. British combinations (rhubarb-custard, English garden blends) appeal to UK consumers.

These aren't gimmicks. They're authentic stories from European culinary traditions. Local brands capturing regional tastes outpace global brands offering uniform positioning. This is particularly true in Germany, France, and Nordic countries where "local" and "authentic" carry premium weight.

What This Means for European Brands

The European kombucha market entering 2026 rewards brands that understand three realities.

Hospitality comes first, retail follows. The American model of retail-first, hospitality-secondary doesn't apply. Build café, restaurant, and bar relationships. That's where European consumers discover brands. Retail becomes easier once hospitality establishes credibility.

Regional strategy matters more than pan-European uniformity. Germany wants "bio" certification and targets 30-50 year olds. The UK wants alcohol alternatives for millennials. France wants sophisticated café positioning for younger demographics. Imposing uniform positioning across Europe guarantees you'll underperform local competitors everywhere.

Authenticity defends against functional soda disruption. Olipop and Poppi are coming with American capital and distribution muscle. But European kombucha has centuries of fermentation tradition, actual live cultures, and cultural credibility that mass-market American sodas can't replicate. Articulate that difference before they establish beachheads.

The opportunities are accessible for brands willing to adapt for European market realities. The category is growing. But the strategies that win look fundamentally different from North American playbooks.

Explore our full range of fermented beverage solutions designed for European commercial producers.

Download our free Kombucha Troubleshooting Guide for production insights.

Frequently Asked Questions

-

Europe's kombucha market reached approximately €905 million (USD 1.02 billion) in 2025, growing at 13.4% CAGR. Germany dominates with 20.1% market share. France is the fastest-growing market at 15% CAGR.

-

European distribution is café-first, with hospitality accounting for 60.8% of sales versus North America's retail-dominated model. European consumers discover kombucha on-tap at cafés and bars before purchasing for home. Regional preferences matter dramatically more. Germany targets 30-50 year olds prioritising "bio" certification. UK wants alcohol alternatives for millennials. France seeks sophisticated café positioning.

-

France leads at 15% CAGR, projected to reach USD 379 million by 2033. Eastern Europe (Czech Republic, Poland, Romania) shows 22% growth from a smaller base, representing frontier opportunity. Spain (18%) and Nordic countries (16%) also accelerate rapidly.

-

Functional sodas like Olipop and Poppi are entering UK and German markets. PepsiCo's 2025 acquisition of Poppi (USD 1.95 billion) signals serious European expansion plans. But European kombucha has defensible advantages: authentic fermentation tradition, actual live cultures, and cultural credibility that mass-market American sodas can't replicate.

-

Research shows demand elasticity around €3.00. Brands at €2.50 to €2.99 see significantly higher velocity than premium competitors at €3.50 to €4.50. However, premium pricing (€4.00 to €5.00) still works in European hospitality channels where consumption context justifies it. Channel-specific pricing matters more in Europe than North America.

-

60.8% of European kombucha distribution flows through cafés, bars, and restaurants. European consumers discover kombucha in social settings first, then seek it in retail. Brands without hospitality presence struggle to build awareness in markets where 60% of consumers still don't know what kombucha is. The discovery journey is opposite from North America's retail-first model.